I have been M.I.A. for a while….

It’s been a crazy time for all of us, I hope that this note finds you and your family healthy and safe. As some of you know, I manage about $3 billion across multiple asset classes including global equities, global fixed income and alternative assets. The last two months have been extremely busy with strategy calls, manager calls, cash movements, Board meetings, etc.

This past weekend I had a little down time, so I am excited to finally have a moment to put together another MacroCrunch, I hope that you enjoy it.

BLACK SWANS:

So where did we leave off?

The last piece I wrote was on March 13, 2020, it was titled The Black Swan of 2020, check it out if you missed it.

In a recent New Yorker article Nassim Taleb said that the recent events were not a Black Swan, but rather a White Swan. That is to say that policy makers could have and should have seen the pandemic coming. Maybe Nassim is right, but I am pretty sure that most investors in the United States and Western Europe would agree that we all underestimated the impact on markets and most certainly the ensuing economic and social paralysis the pandemic has caused. It is truly an unprecedented event in our lifetime.

I first wrote about Covid-19 in the February 11, 2020 issue of MacroCrunch. I thought that it was having a devastating impact on Hong Kong and China, but I did not connect the dots on how contagious the virus was and how quickly it would spread around the world. My modeling was based on the 2002 SARS-CoV outbreak (73 cases in the US) and the 2012 MERS-CoV (2 cases in the US). In hindsight, clearly not the right data sets….. I should have watched Bill Gates 2015 TED Talk.

Netflix also released a great documentary, the Coronavirus Explained, I highly recommend it if you haven’t already seen it.

CENTRAL BANKS vs. COVID-19:

If you have been following MacroCrunch, you know that I have been spending a lot of time on the zero interest rate policy (ZIRP)/ quantitative easing (QE) and the impact these policies have on markets. In general, it is very difficult to take the other side of central banks adding liquidity in the form of lower interest rates and QE. For more background on this check out Negative Yields and Inverted Yield Curves. Fighting the Central Banks, to use an old trading analogy, is kind of like picking up nickels in front of a steam roller.

There is an epic battle occurring between the Covid-19 economic paralysis and Central Banks ZIRP and QE policies meant to offset the damage. I believe that this relationship underpins the disconnect between the economic data being reported and the markets recent performance.

Below is a chart illustrating the announced central bank QE programs and the forecasted bond purchases. These are massive programs and if you missed Fed Chairman Jay Powell’s 60 Minutes interview last weekend he said that there is plenty more where that came from if needed. (chart is courtesy of JP Morgan).

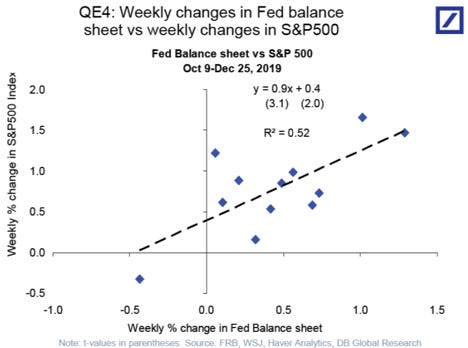

When the Central Banks add $5 trillion in capital to the the markets it pushes all investors out the risk curve in search of higher returns. This is because Central Banks’ purchases of bonds artificially reduce yields, which then forces their natural buyers to seek higher returns elsewhere. Below is chart that I have posted in the past which shows the correlation between the Federal Reserves balance sheet and the S&P 500.

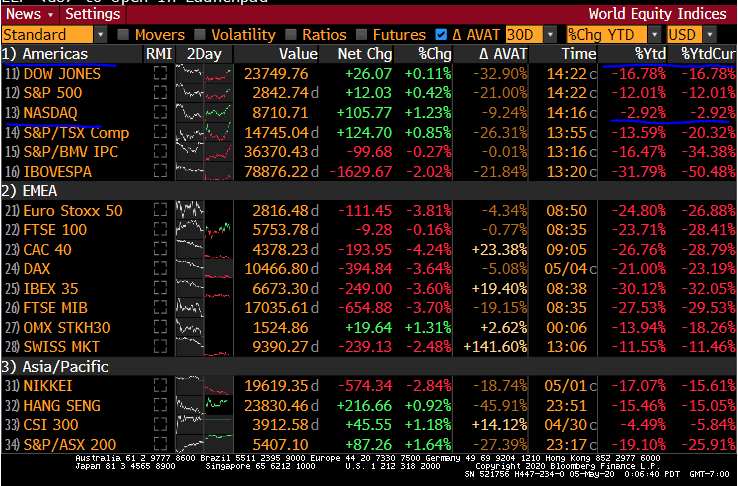

When scanning the global equity indices on my Bloomberg I noticed that the US markets are significantly outperforming all other markets. In fact the snapshot below is a bit stale as the NASDAQ is now up 6% YTD and the S&P500 is only down 8% YTD. This could be as simple as the USA is the least dirty shirt in the hamper, i.e. it is the best alternative.

Another possibility of why the US markets have such a strong relative bid could be our position as the reserve currency of the world. Put simply, there are a lot of dollars all over the world seeking a return. The sovereign wealth funds that I visited in Dubai and Abu Dhabi told me that roughly 60% of their portfolio was invested in the United States. If you are interested in the composition of FX reserves check out the BIS report and the chart below.

There has been a lot of discussion on negative rates and whether or not that could ever happen in the United States. Rates are negative in Japan and certain European countries. I don’t think that the Fed will take rates into negative yields, but never say never as the Fed Funds futures went negative last week!

Check out Dr. Lacy Hunt’s recent interview on the Financial Repression podcast, it is pretty interesting and I highly recommend the Van Hoisington Investment Management quarterly updates on the treasury markets, I read them religiously.

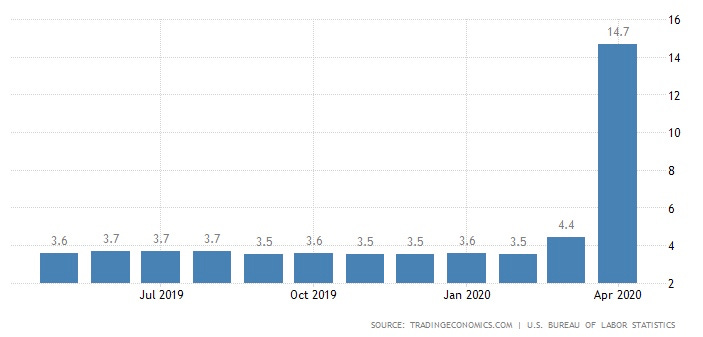

Contrast the above with the recent economic data coming out of the United States and you can see why many are scratching their heads when they look at the current market environment. Real GDP declined 4.8% in Q1 2020, Unemployment hit 14.7% in April, Retail Sales were down 16.4% and industrial Production was down 11.2% in April, etc.

USA Real GDP:

USAUnemployment Rate:

USA Retail Sales:

USA Industrial Production:

So the economic fundamentals look really bad, worse than what we saw in the GFC of 2008/09. But investors seem to be looking through this data and anticipating a rather quick recovery. Check out Mohamed El-Erian’s interview with Chris Wallace on the Fox News Sunday broadcast, he thinks that we will not see a V shaped recovery but rather it will be a W shaped recovery. I think that makes a lot of sense.

Personally, I have used this rally to raise some cash. If I am wrong and the market makes a new high I’ll put that cash back to work. But for now, I see this as an opportunity to transfer some risk from my balance sheet to the Fed’s. If the market wobbles I’ll be in a good position to take advantage of it.

SHOW ME THE MONEY:

After all of the above, I want to close on a lighter note….

How do today’s hedge fund managers stack up against entertainers and CEOs?

It’s not even close…… Meb Faber of Cambria Investments put out a chart using 2016 data and as you can see below there really is not comparison. The hedgies are masters of leveraging Other People’s Money (OPM) to take advantage of Zero Interest Rate Policies (ZIRP) and Quantitative Easing (QE) in the form of inflated financial assets.

I hope you enjoyed the letter and as always feel free to share it with friends and colleagues. If you are interested in startups you can join over 750 other backers that follow my syndicate here.

Be well and stay safe. - Sean Bill / MacroCrunch