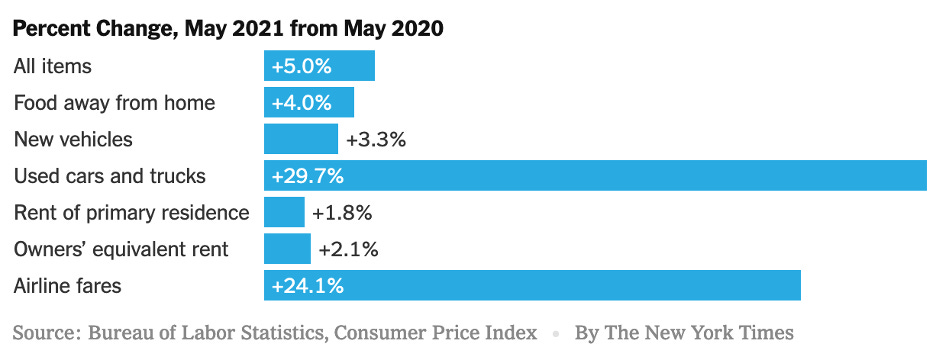

Last week we got an update on inflation. In the United States the headline consumer price index (CPI) rose 5.0% verses a year ago, and the core index, which excludes food and energy, rose 3.8%, the largest 12-month increase since 1992.

But, it should be noted that the year over year comparisons were starting from a very low base that coincides with the beginning of the pandemic (see chart below). As we enter the fall the Y.O.Y. comparison should normalize.

Which leads to the debate that has been raging within the fixed income community on whether the current rise in inflation is transitory in nature or more permanent?

Both sides can make a logical argument for their case. If you are in the transitory camp you point to pent up demand resulting from the pandemic. If you are in the permanently higher camp you point to unrestrained government spending and the expansion in the money supply.

Both are well rooted arguments.

But last week’s data seemed to tilt the argument in favor of transitory inflation. Last week’s uptick in inflation was largely driven by short-term supply constraints and technical dislocations. Car rentals, airfares, food away from home (restaurants), and hotel prices all experienced sizable increases.

The most interesting data we saw was on the used-car market. Used-car prices rose sharply, increasing 7.3% in May from April or 29.7% verses a year ago (see chart below), which accounted for about one-third of the overall increase in inflation for the month of May.

We have all heard about the shortage of semiconductors for new automobiles and the shift away from mass transit to individuals driving themselves to work. All of this has created an increased demand for used automobiles.

I decided to test the market and entered the necessary info on Carvana and Vroom to get a bid on my 2014 BMW i3. I have to say that I was pleasantly surprised at the number and decided to sell the car to Carvana; the Vroom bid was just a couple hundred dollars less. Pickup is scheduled for this Wednesday.

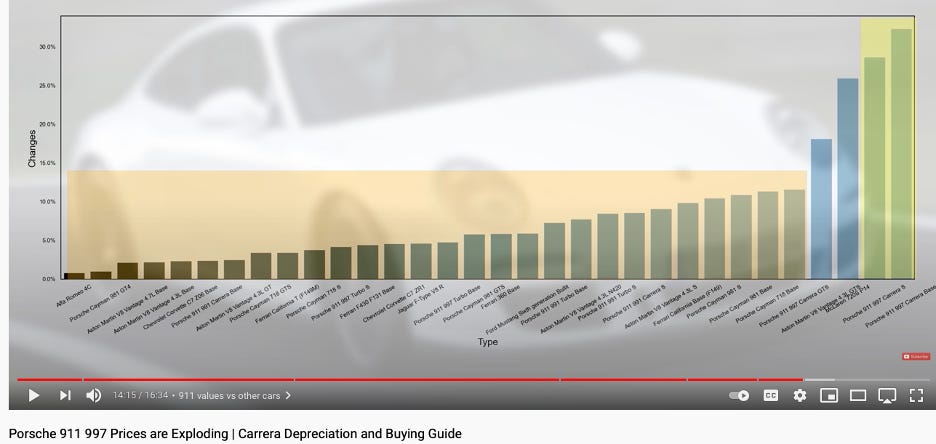

Side note, the market for used Porsche 997s is going bonkers, up 30 - 40% Y.O.Y.

But back to inflation…..

A couple other things that stand out to me. First, government bond yields fell to their lowest levels in three months, and are back below pre-pandemic levels. That tells me that market sentiment is shifting from fear of runaway inflation to the belief that price pressures are transitory and will soon subside.

But even more interesting is that TIPS break-even inflation spreads are holding at 10 year highs while nominal rates are heading lower again. This looks like a good risk reward trade for a break even spread tightener position. But proceed with caution / stop losses as the central banks are likely distorting markets with their massive QE programs.

PODCAST:

PLANET MONEY - USED CAR TALK: Demand for used cars decreased in the first few months of the pandemic as travel came to a sudden halt. But some people still needed to go to work, and they wanted to avoid public transit for their own safety. Those working remotely realized that working from home could be done anywhere. People wanted to buy used cars again, but where had all the clunkers gone?

I hope that you enjoy the letter as much as I enjoyed making it and please feel free to share the links with friends and associates and if you are interested in startups and are an accredited investor you can join over 750 other backers that follow my AngelList syndicate here.

Be well and stay safe. Sean Bill / MacroCrunch / Twitter