Friday morning the markets breathed a sigh of relief, inflation in the United States did NOT break 7.00% on a year over year basis, victory!

For the rest of us an increase of 6.80% is still rather unsettling. So I thought I would take a look at where we are in a historical context and what assets may outperform in an inflationary environment.

From a historical standpoint, Friday’s inflation numbers are the highest Y.O.Y. numbers since 1982, almost 40 years ago when Paul Volcker was beginning to get the 1970s runaway inflation under control. The chart below, courtesy of Bloomberg, shows headline and core inflation over the last 40 + years.

The chart below goes back a little further, which is helpful for context.

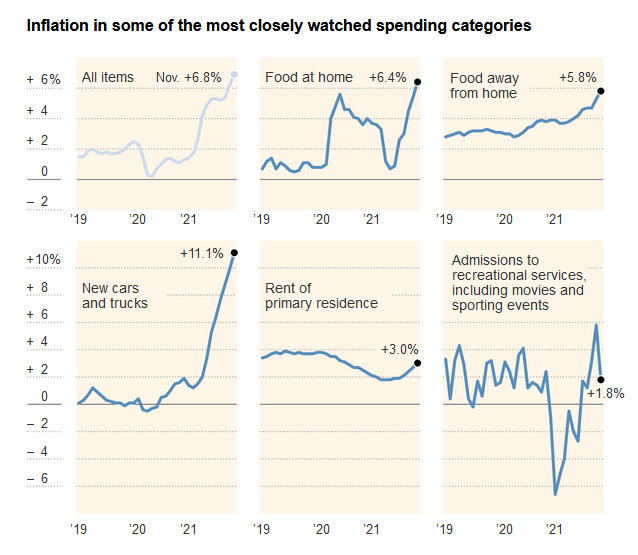

What’s driving the current increase in inflation? The story hasn’t changed much, it is autos, energy and less so food.

Below is a breakout from the NY Times on some of the key sub-sectors driving inflation. The area that is of particular interest to me is the survey of rent of primary residences. I’ll come back to this.

Bloomberg’s models indicate that we may be near the peak of inflation and that they expect inflation rates to normalize in 2022 / 2023 as supply chains return to normal. This will be highly dependent on how Covid and policy responses to Covid evolve.

One area that does concern me is that there is a disconnect between housing prices and survey results. VanEck published an interesting chart showing the lag between housing prices and CPI, it seems like a reasonable assumption that we can expect the housing component of CPI which is 33% of the index to continue to add inflationary pressure.

That said, I do think that what we are seeing here is largely driven by dislocations in the economy that are a result of the pandemic and government policy responses and that over time supply and labor disruptions will normalize. But I don’t think this self-corrects in the next 6-12 months, I think inflation is sticky and it will be with us for the next 1-2 years.

Looking beyond 1-2 years I think that Lacy Hunt’s scenario comes back into play and that the longer term risk will be disinflation and debt deleveraging. I included the interview with Lacy Hunt below in the podcast section in case you missed it in my last note.

INFLATION MITIGATION:

So if we have sticky inflation for the next 1-2 years, what are some assets that may help mitigate the damage to our purchasing power?

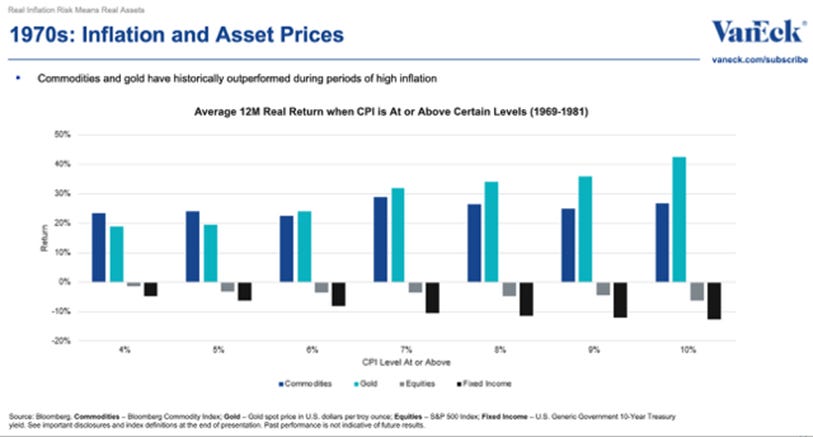

VanEck published some interesting charts on how assets performed in the 1970s and 2000s inflation episodes. They also put together a great webinar which I have included in the podcast section below.

In the 1970s Gold and Commodities outperformed. Both equities and fixed income lost ground on a real return basis as inflation exceeded 10.00%.

In the 2000s inflation levels did not reach the 1970s highs, so really fixed income was the only category that lost ground on a real return basis as inflation only briefly exceeded the 5.00% threshold.

Today’s numbers have opened the door to looking more closely at the 1970s for guidance as we have exceeded the inflationary levels seen in the 2000s.

One last chart to consider….. the growth in Bitcoin versus Gold ETFs is interesting. I am not saying that all gold held by investors is in the form of ETFs, but ETFs are an easily accessible way for retail and institutional investors to hold gold. What stands out to me here is that we are not seeing a big increase in the demand to hold gold via ETFs, but we are seeing a steady increase in the value of Bitcoin.

I think a lot of sophisticated investors are choosing Bitcoin over Gold as an inflation hedge. Bitcoin offers a fixed supply, that is easily transferable and so far has been unhackable. In the meantime central banks have been printing money like drunken sailors.

PODCAST:

YouTube Interview with LACY HUNT: Inflation today, deflation tomorrow.

In this episode Lacy Hunt, one of the world’s top experts on the inflation / deflation makes a very compelling argument why the spike we’re seeing in inflation today will likely be short-lived, and that deflation remains the bigger threat.

Hat tip to Jelly Donut on Twitter for sharing this one, definitely worth a follow!

Real Inflation Risk Requires Real Assets: Lara Crigger interviews David Schassler, Portfolio Manager and Head of Quantitative Investment Solutions for VanEck.

Many investors have never experienced the destructive portfolio impact high inflation can inflict. Investors last faced inflation risk in the early-to-mid 2000s, with the most notable bout of inflation occurring in the 1970s. Over the last several months, the inflation debate has evolved from whether there would be any inflation at all to how high and how long it will last. As a result, the need for investors to reconsider their portfolio exposures has taken on even more importance.

CONFERENCES:

No more conferences until 2022. I plan to use the down time to catch up on my reading list.

I hope that you enjoy the letter as much as I enjoyed writing it and please feel free to share the links with friends and associates. If you are interested in startups and are an accredited investor you can join over 750 other backers that follow my AngelList syndicate here.

Stay safe and stay well. Sean Bill / MacroCrunch / Twitter